The Gold market has broken out of the bearish stance temporarily. Gold is a wonderful safe-haven currency that may hedge against inflation and/or currency devaluation. The currency devaluation in China potentially may trigger further reevaluations of each global currency. In the stock valuations, it may be a matter of overvaluations that may be necessary to reign in irrational exuberance in the market. We do have a potential perfect storm for Gold in the case that the Ukraine situation heats up. If the Iranian Diplomat refusal ignites further conflict with Iran. If the Stock Indices do not bottom soon. If the US Dollar becomes more devalued. Any of these conditions may result in a takeoff of the Gold market. The accommodative stance of the Fed and the further out the tightening may also support the Gold market somewhat. The more dovish the Fed, the better for Gold. The US is constantly in the spotlight and while the US Dollar remains a premier currency, countries may dump dollars for other products that may be a stronger performer. While all of these factors could potentially lead to a higher Gold price, none have come to fruition to the point that we would need for the Gold to takeoff, so we may experience again a range bound market in the near-term. Central banks are still net buyers of the Gold with holdings increasing 6.3 million ounces last year. The banks are projected to buy 5.4 million ounces in 2014. The industrial demand for Gold has reached about 92.0 million ounces in 2013. Investment demand had decreased to 30.9 million ounces in 2013. The Central Bank of Iraq had acquired 36 metric tons of Gold in March. Central banks purchased 544 tons of Gold in 2012 without the data or excluding China while in 2013 went to 369 tons. China rarely releases data to get a view of their holdings. Germany is currently moving Gold from New York to Frankfort in an attempt to increase their reserves while their holdings are the second largest to the US at 3,387.1 metric tons. Mexico had increased their holdings by 78.5 tons of Gold in March. Kazakhstan February reserves at 4.73 million troy ounces. The US reserves 8,133.5 tons. Holdings in the SPDR Gold Trust increased 0.6 % to 821.47 metric tons. Supplies of Gold above ground are estimated to be about 177,200 tons according to the World Gold Council. Gold remains as one of the most liquid assets that has rallied in the face of the worst calamities in our history books.

The fear factor was ignited further today taking the VIX to 17.03! The Treasuries also have benefited over the high anxiety in the marketplace taking the long-bonds up to $134^28. The valuations of the stock do not justify the share prices. No longer can inclement weather conditions suffice for missed targets. Now the harsh reality sets in to reevaluate the stock prices of individual stock on merit. Allocations may shift as portfolio adjustments are made. There may be bargain hunting where investors may look for smaller companies with good market capitalization or just quality, making it more of a stock pickers market. Some major companies valuations and revenue growth just were not there. To add to the concerns, China’s imports and exports were down in March contributing further to the weakness. Premier Li Keqiang states that more tools may be used to increase growth. To add to the apprehension, the International Monetary Fund (IMF) Managing Director Christine Legarde retorts that rebalancing is the intention of the Chinese Yuan depreciation yet other countries such as the US have been opposed. The Yuan was set to depreciate before widening the exchange-rate band on March 17th. China does want their currency to become a reserve currency in the future yet the recent import/export numbers do not support a higher Yuan. Exports decreased 6.6 % while Imports decreased 11.3 % to a trade surplus of $7.71 billion. The devalued currency will help the country’s exports as they become cheaper to purchase. China’s projected growth rate is set for 7.5 %. The US already has concerns about a devalued Yuan making goods from China less costly and more appealing to global consumers. The US appealed to the G-20 on deaf ears as the Euro Zone, Australia, Canada, New Zealand and Japan have been trying to devalue their currencies. The US Federal Budget Deficit came in at $36.9 billion while a year ago it was $106.5 billion. The taxes were up while the spending was down. The sequestration and higher revenue got rave revues by the IMF. Last October, the US was close to suffering a default but managed to draw up a budget agreement temporarily. They still need the long-term sustainable agreement drawn up that would enrich the nation beyond a potential deficit. Treasuries increased after the Fed minutes this week as the market may have had tightening expectations dampened. The increased time on the tightening may have boosted the Treasuries at the Indexes expense. The increase may take place more likely mid-to-latter-2015. The US Fed released the minutes of the March 18th – 19th Fed meeting Wednesday. US Fed Chairperson Janet Yellen had regained the positive vibe as she said that the US has a “considerable slack” in the labor market allowing the accommodation to remain as back up for some time to come. Her commentary prior had put a potential tightening on interest rates in perhaps as little as six months. She was able to calm investors with a dovish tone. Projections for continued growth in the US look extremely positive with little to drag it down at this time. US Fed Chairperson Yellen keeps the accommodative stance as a floor for this market, by maintaining that the Fed may have further tools or at least implying that. The International Monetary Fund (IMF) and the World Bank along with financial ministers and world bank governors are to meet April 11th thru the 13th to discuss economic issues and financial markets. IMF Managing Director Christine Lagarde coined the word “Low-flation” as she asked for additional monetary easing in the Euro Zone and Japan. The Euro Zone’s gauge of economic confidence gained to 102.4 in March while the previous reading was 101.2. The US interest rate projections by analysts are from 4.25 % to possible 3 % to the end of 2016. The European Central Bank met with an unchanged interest rate, yet they did discuss a potential stimulus. The German IFO Business Conditions Index decreased in March to 110.7 while the previous reading had been 111.3. The European Central Bank is contemplating a program of quantitative easing much like the US had to thwart a deflationary passage. The Bank of Japan on the other hand may be introducing further stimulus with deflation concerns. The IMF sees the world economy growth at about 3.6 %. The IMF sees the Euro Zone with a 2.9 % GDP this year. The Bank of England officials state that they will maintain the key interest rate at the lows until Employment decreases from 7.2 % to 7.0 %. The IMF is projecting the US growth to 2.8 % this year and 3.0 % in 2015. Russia and economic sanctions may be discussed. Russia is cited for the sanctions but they may target more than the giant economy as US companies have investments in Russia such as Boeing and General Electric. The Euro Zone including Germany may also suffer as the sanctions are imposed on Russia to put a financial strangle hold on the country. A snowball effect of conflict could ultimately result in the sanctions as Russia has been playing an integral part of negotiations with Iran on the nuclear program. Sanctions on Iran had been previously placed to pressure the country into allowing the NATO inspectors to come into their nuclear facilities to monitor the use of uranium. The uranium is said to be used at the highly developed level for medical purposes but it also becomes capable of being used to complete a nuclear bomb. Israel is within reach to Iran to suffer any hostile action initially and therefore they have pressured the US to propose the sanctions. Iran is now anxious to wind up the talks and agreements. US President Obama now wants to prevent the Iranian Ambassador, Hamid Aboutalebi from entering the US as the chosen UN envoy. He had been involved with terrorist activity in the past and the president feels him a threat to US safety. In 1979, the takeover of the US embassy was credited to the ambassador as one of his espionage efforts. He may be denied a US Visa to work at the UN. US President Barack Obama has been under some pressure for perhaps not opposing the takeover of Crimea by Russia more, but his diplomacy is of the utmost importance in such matters. Russian President Putin further taunts the US with support for Bashar al-Assad in Syria. They have sent weaponry like the “vacuum bomb” which is a heat and pressure explosive device. Iran and Russia are both with sanctions bartering goods and using oil to gain the products necessary for survival. The global relationships are vital to maintain peace and harmony. The nuclear disarmament of Iran and the role that Russian President Putin has is of vital importance to world peace. Putin can use his close relationship to the Iran officials to maintain harmony and keep the talks open. Russia is a huge trade relationship where globally, it would make a difference to other countries if the sanctions against Russia were to tighten. On the Russian developments, Vladimir Putin announced that he is not intent on splitting up the Ukraine. He is bent on increasing the region’s profitability with tourism and as an energy route. For the people of Crimea, much will change. Ukraine people will need a Russian Visa to travel within the region. The Russian leader is invoking some sanctions of his own as the Ukraine purchases about a half of their natural gas from Russia. OAO Gazprom (GAZP) is the primary Russian gas export firm that is owed at $2.2 billion by the Ukraine. Russia feels it is within their right to revert to a prepay account with the Ukraine. Gazprom recently increased their prices substantially to the Ukraine perhaps in the heat of the potential conflict regarding Crimea. Global leaders are looking for a resolve perhaps even a possible reverse flow system from Eastern Europe. April 17th, global leaders meet in Geneva to look for solutions. The vote was in favor of Crimea to secede and ask the Russian Federation for Membership. Crimea had belonged to Russia back in the 1954 until Nikita Khrushchev had given the Black Sea region to the Ukraine. Russian President Putin defends his right to send troops to the Ukraine on behalf of the Russian citizens residing there. He actually stayed within the treaty limit of 25,000 troops initially, but it was reported that about 40,000 troops remain around the Ukraine border. The Ukraine is seeking financial aid from the IMF of up to about $18 billion to help the country out of the debt. The G-7 is to discuss the Ukraine situation in Washington. The G-7 consists of the US, Japan, Germany, UK, Italy, France and Canada. Global leaders still regard Russia’s action as grabbing a country for benefits perhaps derived from the resources of the region. World leaders are intent on watching Putin to be sure his “annexing” stops at Crimea! British Prime Minister David Cameron regarded this action as a breach of international law. Sanctions may be imposed on Russia still yet regarding this action such as travel bans and financial sanctions. About $5.5 billion of outflows have already transpired this year in Russia in light of the sanctions. US sanctions have already stopped the Visa and MasterCard services at the Bank Rossiya in St. Petersburg. Sanctions on parties in Putin’s inner circle have been targeted. The sanctions have already had an impact on Russia as Fitch’s credit rating agency has cut the outlook to BBB negative. Loans have been called in and gold reserves have fallen to $493.2 billion as of March 14th. The G-8 said that they will suspend the G-8 Summit in Sochi this year. The Organization for Economic Cooperation and Development has spoken of revoking Russia’s entrance into the organization. Asset blockades, financial and trade sanctions have all been suggested. Putin may pay about $3 billion ++ costs to annex Crimea. The problem seems to be a history of violating international boundaries for the Russian President. Putin retorts that the US and NATO have come close to the Russian borders. For the moment, the market is taking Putin’s words as peaceful! If or when sanctions are imposed by other countries, will the environment remain peaceful or could another cold war escalate? For now, Putin seems to be concentrating on the completion the annexing of Crimea. Russia and the US had fought on the same side during WWI and WWII yet tensions still run very deep. Russian troops seized the Crimean port of Sevastopol raising their flag. Russia’s take-over of Crimea will perhaps consist of pension adjustments up to the Russian pensions, raises, infrastructure upgrades such as quite possibly a bridge and a tunnel. The EU may proceed to lighten imports of natural gas from Russia. It is hopeful that the Russian President will be able to show that he is not interested in taking other regions and that his intent is peaceful. It would be also hopeful that the sanctions would not constrict to the point of pressure to escalate any aggression. The Euro Zone and the world would feel the pressure of the sanctions as many global workers are employed by Russian companies. Russia and the US both have an accord on nuclear terrorism threats realizing that international cooperation is necessary to provide a stronger front.

Today’s Producer Price Index for March was 0.5 % while the previous reading had been -0.1 %. The PPI excluding food and energy was 0.6 % while the previous reading was -0.2 %. The PPI excluding food, energy and trade services was 0.3 % while the previous reading was 0.1 %. The PPI Goods were 0.0 % while the previous reading was 0.4 %. The PPI Services were 0.7 % while the previous reading was -0.3 %. The Consumer Sentiment for April was 82.6 while the previous reading was 80.0. The Initial Jobless Claims for the week of April 5th was down 32,000 to 300,000 while the previous reading had been 326,000. The Continuing Claims was down 62,000. Import Prices for March were 0.6 % while the previous reading had been 0.9 %. The Export Prices were 0.8 % while the previous reading was 0.6 %. The Bloomberg Consumer Comfort Index for April was -31.9 while the previous reading had been -30.0. The Treasury Budget for March was -$36.9 billion while the previous reading was -$193.5 billion. The Fed Balance Sheet of Total Assets was $7.7 billion while the previous reading had been $9.5 billion. The Reserve Bank Credit was $6.9 billion while the previous reading was $4.7 billion. The Money Supply for the week of March 31st was -$37.0 billion while the previous reading had been $20.0 billion. The MBA Purchase Applications Composite for the week of April 4th was -1.6 % while the previous reading was -1.2 %. The Purchase Index was 3.0 % while the previous reading was 1.0 %. The Refinance Index was -5.0 % while the previous reading was -3.0 %. Wholesale Trade Inventories for February were 0.5 % while the previous reading was 0.6 %. The Federal Open Market Committee minutes were read today from the March 18th and 19th meetings. The Fed expressed that policy will remain loose for years and the tapering is in measured steps supporting the stock indices. A couple of Fed members see the Fed Funds Rate low as inflation remains below 2 %. The NFIB Small Business Optimism Index for March was 93.4 showing increased confidence in the economy while the previous reading was 91.4. The ICSC-Goldman Store Sales for the week of April 5th was 1.5 % while the previous reading was 3.6 %. The Redbook Sales for the week of April 5th was 2.9 % while the previous reading was 2.3 %. The JOLTS (the Labor Department’s Job Openings and Labor Turnover Survey for February was 4.173 million while the previous reading was 3.974 million. The Gallup US Consumer Spending Measure for March was $87 unchanged. The TD Ameritrade IMX for March was 5.87 while the previous reading was 5.74. US Consumer Credit for February was $16.5 billion while the previous reading was $13.7 billion. The Nonfarm Payrolls for March was 192,000 while the previous reading was 175,000. Though better than February’s report, the forecast of 206,000 left some traders disappointed with the moderate number. The Unemployment rate was left unchanged at 6.7 % while the forecasts were for 6.6 %. The Average Hourly Earnings was 0.0 % while the previous reading had been 0.4 %. The Average Workweek was 34.5 hours while the previous reading was 34.2 hours. The Private Payrolls was 192,000 while the previous reading was 162,000.

This is where the long-term safe-haven qualities must be viewed to determine the true value of Gold. It is not the type of commodity that is typically day-traded. Its true purpose is as a currency when others are devalued. It is a hedge against inflation. It is a backup plan for a world in conflict or crisis. It is the type of investment that one may not need all the time but when an event takes place, it is worth its weight in Gold.

The Gold (June) contract is in buy mode if it stays above $1282.40. It could retrace to $1186.70 or back up to $1392.20 depending on the Ukraine situation and the economy. A key consolidation area may be $1318.90. The range may be $1307.00 to $1350.00 for now. Should Russian President Putin become ambitious to acquire additional annexing of the neighboring regions, nuclear talks begin to fail, the economic reports detect a contraction of growth in the US and/or a slowdown in China all could spur positive price action in the Gold market back to the old highs or above. For now, the Gold carries a negative positioning remaining under pressure. Anything can happen. The options may give a trader the right to control a futures position at a specific price or to simply profit/loss on the premium itself. It is suggested to consult your broker without delving into options if you are unfamiliar with them.

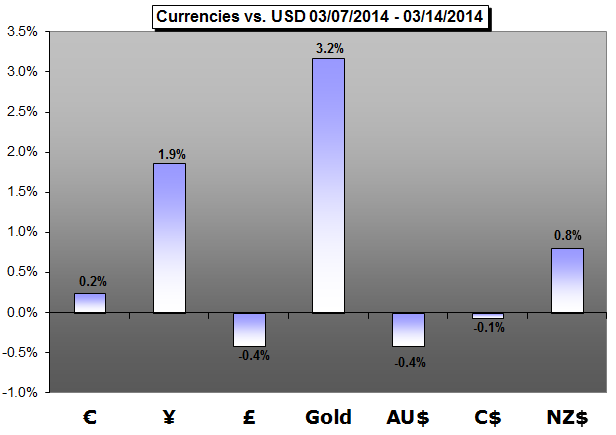

Gold Chart

--